Excellent study material for all civil services aspirants - being learning - Kar ke dikhayenge!

Corporate governance - Part 2

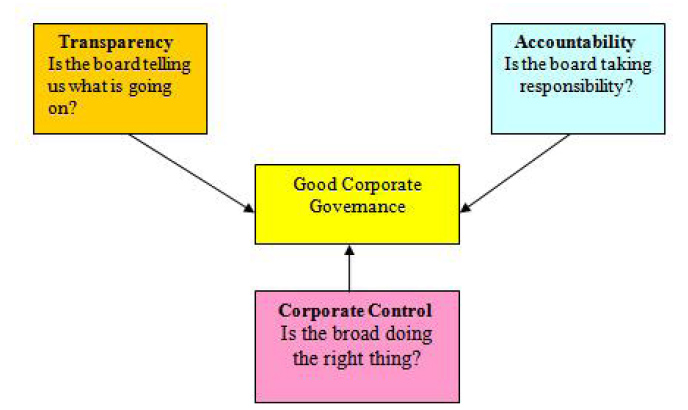

4.0 Mechanisms and controls

A corporate governance structure combines controls, policies and guidelines that drive the organization toward its objectives while also satisfying stakeholders' needs. A corporate governance structure is often a combination of various mechanisms. The mechanisms and controls are designed to reduce the inefficiencies that arise from moral hazard and adverse selection.

4.1 Internal mechanism

The foremost sets of controls for a corporation come from its internal mechanisms. These controls monitor the progress and activities of the organization and take corrective actions when the business goes off track. Maintaining the corporation's larger internal control fabric, they serve the internal objectives of the corporation and its internal stakeholders, including employees, managers and owners. These objectives include smooth operations, clearly defined reporting lines and performance measurement systems. Internal mechanisms include oversight of management, independent internal audits, structure of the board of directors into levels of responsibility, segregation of control and policy development.

4.2 External mechanism

External monitoring of managers' behavior, occurs when an independent third party (e.g. the external auditor) attests the accuracy of information provided by management to investors. External control mechanisms are controlled by those outside an organization and serve the objectives of entities such as regulators, governments, trade unions and financial institutions. These objectives include adequate debt management and legal compliance. External mechanisms are often imposed on organizations by external stakeholders in the forms of union contracts or regulatory guidelines. External organizations, such as industry associations, may suggest guidelines for best practices, and businesses can choose to follow these guidelines or ignore them. Typically, companies report the status and compliance of external corporate governance mechanisms to external stakeholders. Stock analysts and debt holders may also conduct such external monitoring. An ideal monitoring and control system should regulate both motivation and ability, while providing incentive alignment toward corporate goals and objectives. Care should be taken that incentives are not so strong that some individuals are tempted to cross lines of ethical behavior, for example by manipulating revenue and profit figures to drive the share price of the company up.

4.3 Financial reporting and the independent auditor

Reporting of the corporations financials is primarily the responsibility of the board of directors. The Chief Executive Officer and Chief Financial Officer are crucial participants and boards usually have a high degree of reliance on them for the integrity and supply of accounting information. They oversee the internal accounting systems, and are dependent on the corporation's accountants and internal auditors.

An independent external audit of a corporation's financial statements is part of the overall corporate governance structure. An audit of the company's financial statements serves internal and external stakeholders at the same time. An audited financial statement and the accompanying auditor's report helps investors, employees, shareholders and regulators determine the financial performance of the corporation. This exercise gives a broad, but limited, view of the organization's internal working mechanisms and future outlook.

Current accounting rules under International Accounting Standards and U.S. GAAP allow managers some choice in determining the methods of measurement and criteria for recognition of various financial reporting elements. The potential exercise of this choice to improve apparent performance as is evident from the Enron case, increases the information risk for users. Financial reporting fraud, including non-disclosure and deliberate falsification of values also contributes to users' information risk. To reduce this risk and to enhance the perceived integrity of financial reports, corporation financial reports must be audited by an independent external auditor who issues a report that accompanies the financial statements.

One area of concern was when the auditing firm acts as both the independent auditor and management consultant to the firm they are auditing. This resulted in a conflict of interest which places the integrity of financial reports in doubt due to client pressure to appease management. The power of the corporate client to initiate and terminate management consulting services and, more fundamentally, to select and dismiss accounting firms contradicts the concept of an independent auditor. Changes enacted in the United States in the form of the Sarbanes-Oxley Act (following numerous corporate scandals, culminating with the Enron scandal) prohibit accounting firms from providing both auditing and management consulting services. Similar provisions are in place under clause 49 of Standard Listing Agreement in India.

5.0 MAJOR ISSUES IN CORPORATE GOVERNANCE

Major issues in corporate governance reports have included the role of board, the quality of financial reporting and auditing, directors' remuneration, risk management and corporate social responsibility. In order to clear the above statement I need to expand on these issues in later articles but for now let's examine the major areas that have been affected by the corporate governance.

5.1 Duties of Directors

The corporate governance reports have aimed to build on the directors' duties as defined in statutory and case law duties of directors. These include the fiduciary duties to act in the best interests of the company, use their powers for a purpose, avoid conflicts of interest and exercise a duty of care.

5.2 Composition and balance of the Board

A feature of many corporate governance scandals has been boards dominated by a single senior executive or small 'cabinet of kitchen' with other member of board who are working just as a robot toy. It is possible that a single person may bypass the board directions to meet his own personal interests. The report on the UK Guinness case suggested that the Earnest Saunders' chief executive paid himself a reward of £3million without the consent of other directors.

In the case where the organization is not dominated by a single person, there may be other problem in the composition of board of directors. The organization may be run by a minority group revolve around CEO or CFO and recruitment and appointments may be done by personal recommendations rather than formal system. So in order to run a smooth business a board must be balanced in sense of talents, skills, and competence from numerous specialisms related to the organization's situation and also in terms of age (in order to ensure that senior directors are bringing on newer ones to assist in the planning of succession).

5.3 Remuneration and reward of Directors

Directors being paid excessive bonuses and salaries have been identified as significant corporate abuses for a large number of years. It is, however, unavoidable that the corporate governance codes have been targeted this significant issue.

5.4 Reliability of financial reporting and external Auditors

Financial reporting and auditing issue are seen more critical to corporate governance by the investors because of their main consideration in ensuring management accountability. It is the reason that they have been must debated and the focus of serious litigation. Whilst considering the corporate governance debate only on reporting and accounting issues is insufficient, the greater regulation of practices such as off-balance sheet financing has directed to greater transparency and a reduction in risks faced by investors.

The necessary questioning may not be carried out by external auditor from senior management because the auditors may have threat of loosing audit assignment. In the same way internal auditor may not ask an alien question to senior member because their employment matters are determined by the CFO. But generally the external auditors become the reason of corporate collapse, for instance in the case of Barlow Clowes that was poorly focused and planned audit failed to determine the illegal usage of monies from clients.

5.5 Board's responsibility for risk management and internal control

If the Board does not arrange the regular meetings in order to consider the organizational activities systematically show that the board is not meeting their responsibilities. But this thing also occurred sometime when the board is not provided by full information to properly oversight on business activities. All this mess results in the poor system that may unable to report and measure the risks associated with business.

5.6 Shareholders' rights and responsibilities

Shareholders' role and rights is subject of particular importance. They should be informed about all those information that are material to them because these information may influence their amount of investment. They should also be given the right to vote on policies affecting the governance of organization.

5.7 Corporate Social Responsibility (CSR) and business ethics

The lack of mutual decision and sense of responsibility for businesses and stakeholders has unavoidably turned out the business ethics and social responsibility a significant part of corporate governance debate.

6.0 NEED FOR CORPORATE GOVERNANCE IN INDIA

Since 1991, India went in for full scale liberalisation of economic policies. That brought rapid growth, and a lot of scams bred by opaque policy formation or improper policy implementation. Trust in political and business institutions in India has seen a sharp decline as a series of corruption scandals rocked institutions. The crisis of confidence may seem to be a daunting challenge for regulatory agencies but it can also turn into an opportunity for reform for those wise enough to seize it.

The recent moves of India's capital market watchdog, the Securities and Exchange Board of India (SEBI) to improve corporate governance norms of listed companies must therefore be seen as a welcome step in the direction of reform. But much still remains to be done. Following the recently amended companies law that put the spotlight on corporate governance issues, SEBI’s latest directives can help raise the bar on corporate governance in India if the regulator, in league with stock exchanges, follows up on its tough words with punitive action on erring firms.

The signs are more promising this time. More companies now tend to tap capital markets abroad for funds and manage to benefit from higher corporate governance standards. A small but growing class of activist shareholders has emerged in India, which will add heft to the fight for greater corporate transparency. The ministry of company affairs has come a long way in the path towards greater corporate governance, if the provisions of the recent companies' law are to be taken seriously.